AI-driven personalization is projected to deliver a $250 to $500 billion value uplift in global banking, yet many high-net-worth individuals still worry that more technology means less discretion. That concern is understandable but largely misplaced. The most sophisticated private banks today use technology precisely to protect privacy, sharpen security, and deliver the kind of tailored service that used to require a full team of advisors. This article breaks down how AI, digital platforms, and advanced cybersecurity tools are reshaping private banking, and why the right technology stack actually strengthens, rather than weakens, trust and confidentiality.

Table of Contents

- Technology-driven personalization and client experience

- Security, discretion, and deepfake defense in digital banking

- Digital platforms and global banking: unified client views

- Efficiency, profitability, and intergenerational wealth transfer

- Why real discretion and human oversight matter more than ever

- Explore discreet, secure, and tech-forward banking solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| AI personalization boosts value | Advanced AI enables tailored strategies and increases onboarding efficiency in private banking. |

| Security and discretion are vital | Modern banks prioritize cybersecurity and privacy technologies, addressing rising threats and maintaining client trust. |

| Unified platforms drive global efficiency | Digital platforms deliver seamless, cross-border services for high-net-worth individuals and corporations. |

| IT investment enhances profitability | Banks that invest heavily in technology achieve higher profits and reduced loan default rates. |

| Human oversight preserves trust | Despite tech advancements, personal relationships and discretion remain central to private banking. |

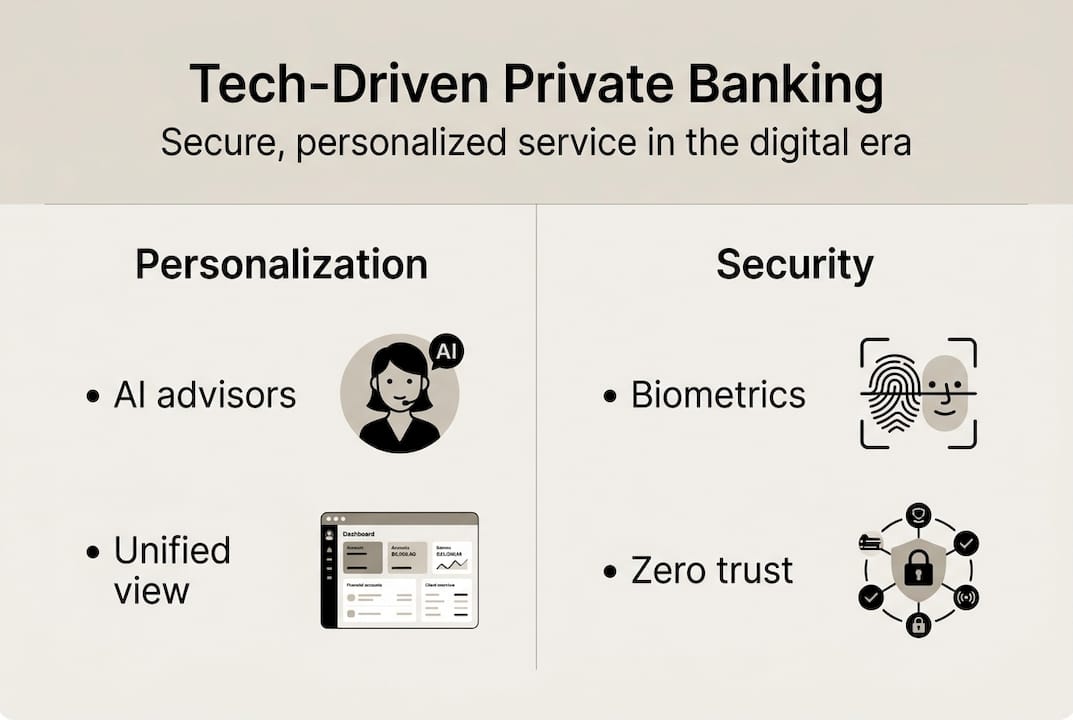

Technology-driven personalization and client experience

For decades, personalization in private banking meant a well-connected relationship manager who knew your preferences by heart. That model still matters, but technology has fundamentally expanded what personalization looks like at scale. AI now handles the heavy lifting of data analysis, freeing advisors to focus on what they do best: strategic guidance and relationship building.

AI automates routine tasks like portfolio analytics, risk scoring, and compliance checks, enabling Relationship Managers to redirect their energy toward nuanced, high-value conversations with clients. The result is faster service, fewer errors, and advice that is genuinely tailored to each client’s goals rather than templated to a segment.

The numbers back this up. Banks with mature AI programs see a 12 to 15% increase in digital onboarding rates compared to peers still relying on manual processes. That efficiency gain translates directly into a better first impression for new clients and a smoother experience for existing ones.

Here is what technology-driven personalization actually delivers for HNWIs:

- Dynamic portfolio construction that adjusts in real time based on market conditions and personal risk thresholds

- Goal-based financial planning tools that map every investment decision to a specific life or business objective

- Predictive analytics that surface opportunities and risks before a client even asks

- Automated reporting that gives clients instant visibility into their positions across all accounts and geographies

This kind of capability is central to the private banking transformation now underway at leading institutions. The shift is not about replacing advisors. It is about giving them better tools so every client interaction carries more weight.

Pro Tip: Even as AI handles more routine tasks, insist that your bank maintains dedicated human advisors for sensitive decisions. Technology accelerates execution, but discretion and trust are still human qualities.

The banks winning in this space are those that have redesigned digital onboarding processes to feel seamless without sacrificing the depth of verification that protects both client and institution.

Security, discretion, and deepfake defense in digital banking

Personalization only matters if it is built on a foundation of real security. The threat landscape for high-net-worth clients has grown sharply more complex. Fraud is no longer just about stolen passwords. AI-generated deepfakes, synthetic identities, and sophisticated social engineering attacks are now targeting wealthy individuals and their advisors directly.

AI-driven fraud losses are projected to reach $40 billion by 2027, making zero-trust architecture and biometric verification essential, not optional, for any institution serving HNWIs.

The response from leading private banks has been to move away from perimeter-based security and toward zero-trust frameworks. Under zero-trust, no user or device is trusted by default, even inside the network. Every access request is verified continuously, not just at login.

Here is how modern corporate banking cybersecurity stacks up against legacy approaches:

| Security dimension | Traditional approach | Tech-enhanced approach |

|---|---|---|

| Identity verification | Password plus SMS code | Biometrics plus behavioral analytics |

| Fraud detection | Rule-based alerts | AI anomaly detection in real time |

| Deepfake defense | None | Voice and video liveness checks |

| Access control | Role-based, static | Zero-trust, continuous verification |

| Incident response | Manual review | Automated containment plus human review |

Beyond the technical controls, the discreet banking advantages of a well-secured digital institution are significant. Clients can transact globally without exposing sensitive information to unnecessary intermediaries. Encrypted communication channels, digital identity credentials, and multi-factor authentication work together to create a private environment that traditional branch-based banking simply cannot replicate.

The key takeaway: security technology is not just a defensive measure. For HNWIs and corporations, it is a core feature of the banking relationship itself.

Digital platforms and global banking: unified client views

For clients with assets, businesses, and interests spread across multiple jurisdictions, fragmented banking is a real operational risk. When your portfolio data lives in five different systems that do not talk to each other, you lose visibility, efficiency, and control. Unified digital platforms solve this directly.

Digital platforms enable unified client views across jurisdictions, giving global HNWIs and their advisors a single, consolidated picture of assets, liabilities, cash flows, and risk exposure in real time. This is not a convenience feature. For complex family offices and multinational corporations, it is a necessity.

The gap between leaders and laggards here is stark. Banks still running legacy core systems carry cost-to-income ratios of 75 to 85%, compared to digitally mature peers operating far more efficiently. That inefficiency has a direct cost to clients in the form of slower execution, higher fees, and more errors.

Regional differences are also significant. Swiss private banks score 39 out of 100 on digital maturity, slightly below the global average of 41, with notable gaps in mobile banking and user experience. Luxembourg-based institutions and Asian private banks are closing the gap faster.

Here is what to look for when evaluating a bank’s digital platform:

- Consolidated dashboards that aggregate multi-currency accounts and investment positions

- Real-time transaction visibility across all jurisdictions

- Integrated compliance tools that handle AML and KYC requirements without creating friction

- API connectivity to third-party wealth management and accounting systems

Pro Tip: When evaluating a private bank, ask specifically about their digital maturity score and platform architecture. A bank investing in unified platforms will serve your cross-border needs far better than one patching together legacy systems.

For clients who need global banking solutions with real-time cross-border execution, premium banking services built on modern infrastructure are not a luxury. They are the baseline. Institutions using SWIFT GPI technology add another layer of speed and traceability to international transfers, reducing settlement times from days to hours.

Efficiency, profitability, and intergenerational wealth transfer

Technology investment is not just about client experience. It reshapes a bank’s entire financial profile, and that matters to clients who want their institution to remain stable and competitive over the long term.

Research shows that banks doubling IT spending see measurably higher profits, increased deposit income, and a 25% drop in loan default rates. That is a direct link between technology investment and institutional health. A bank that invests in its infrastructure is a bank that is better positioned to serve you in five years, not just today.

On the client side, 55% of HNW clients now cite digital capabilities as the top factor when selecting a private bank. That number has climbed steadily and shows no sign of reversing. Meanwhile, legacy systems with cost-to-income ratios of 75 to 85% are a structural drag on service quality and innovation.

The intergenerational wealth transfer dimension adds urgency. An estimated $84 trillion in wealth will transfer between generations in the United States over the coming decades. Younger inheritors expect digital-first experiences. Banks that cannot deliver them will lose assets to institutions that can.

Here are the steps leading banks are taking to stay ahead:

- Migrating core systems to cloud-based infrastructure for speed and scalability

- Deploying AI-driven analytics for real-time risk and portfolio management

- Building mobile-first interfaces that meet next-generation client expectations

- Automating compliance workflows to reduce cost and improve accuracy

- Investing in cybersecurity as a client-facing feature, not just a back-office function

Pro Tip: Explore digital banking advantages before committing to a banking relationship. Institutions already leading in digital adoption will serve your needs better today and adapt faster to whatever comes next.

Why real discretion and human oversight matter more than ever

Here is a perspective that does not get enough attention: the biggest risk in technology-driven private banking is not a data breach. It is the quiet erosion of human judgment.

AI is genuinely impressive at pattern recognition, automation, and efficiency. But technology augments human advisors in private banking rather than replacing them, and the edge cases matter enormously for UHNW clients. Agentic AI systems, which can shift from providing advice to executing transactions autonomously, require a human on the loop at every critical decision point. Without that, discretion becomes a marketing term rather than a practice.

The institutions that earn lasting trust from high-net-worth clients are those that use technology to enhance advisor capacity, not to eliminate it. A relationship manager armed with real-time AI insights is more valuable than either a human advisor working blind or an algorithm operating without oversight.

For family offices managing complex, multi-generational structures, this balance is not optional. The stakes are too high for fully automated decisions. Demand transparency about how your bank blends digital tools with human accountability.

Pro Tip: Ask your bank directly how they handle edge cases and exceptions. The answer tells you more about their culture than any product brochure. Explore the discreet banking perspective to understand what genuine discretion looks like in practice.

Explore discreet, secure, and tech-forward banking solutions

If the standards described in this article resonate with what you expect from a private banking partner, Prominence Bank was built with exactly that client in mind.

Prominence Bank combines advanced digital currency services, secure and streamlined onboarding, and corporate banking solutions designed for complex, global structures. Every service is built on a foundation of discretion, AML/KYC compliance, and real-time digital access. Whether you need multi-currency accounts, institutional asset management, or a clear banking security guide for your organization, the infrastructure is already in place. Reach out to explore how Prominence Bank can serve your specific needs.

Frequently asked questions

How does AI improve personalization in private banking?

AI automates routine tasks like risk scoring and portfolio analytics, freeing advisors to focus on strategic, personalized guidance. Banks with mature AI programs see a 12 to 15% onboarding increase and measurably higher client satisfaction.

What security technologies are most important for private banking in 2026?

Zero-trust frameworks, biometrics, and preemptive AI-driven fraud defenses are the top priorities. AI-driven fraud losses are projected to hit $40 billion by 2027, making these controls essential rather than optional.

Why do global HNWIs prefer banks with advanced digital platforms?

Digital platforms enable unified client views across jurisdictions, simplifying cross-border transactions and giving clients real-time visibility into their full financial picture from a single interface.

How does IT spending correlate with bank profitability?

Banks doubling IT investment see higher profits, increased deposit income, and a 25% reduction in loan default rates, making technology spending a direct driver of institutional strength and client outcomes.