Traditional banks have long been considered the gold standard for managing serious wealth. That assumption is cracking. 55% of HNW clients now cite digital capabilities as a top selection factor when choosing a wealth management provider, signaling a fundamental shift in how sophisticated individuals and corporations think about financial infrastructure. This guide breaks down what digital banks actually deliver, where they outperform legacy institutions, how privacy and compliance work in practice, and what to look for when selecting a provider for complex, international financial needs.

Table of Contents

- What defines a digital bank today?

- Key advantages of digital banking for high-net-worth individuals and corporates

- Risks, privacy, and regulatory realities in digital banking

- Digital versus traditional banks: Efficiency and integration for global finance

- How to evaluate and choose the right digital bank

- Unlock advanced digital banking with Prominence Bank

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Unmatched digital security | Biometrics and AI fraud checks can exceed traditional banks’ defenses for high-value accounts. |

| Rapid global onboarding | Digital banks let you open accounts and get approval much faster than legacy institutions. |

| International transaction ease | Multi-currency accounts and APIs support seamless global management for HNW clients and corporates. |

| Trusted privacy options | With proper due diligence, digital solutions can rival traditional banking for privacy and regulatory compliance. |

| Lower operational costs | Digital banks operate lean, passing efficiency and cost benefits to clients versus legacy providers. |

What defines a digital bank today?

A digital bank is not simply a traditional bank with a mobile app bolted on. It is a fully technology-native institution that operates without physical branches, built from the ground up to handle account opening, transfers, compliance, and wealth management entirely online. That distinction matters enormously for clients who need speed, discretion, and global reach.

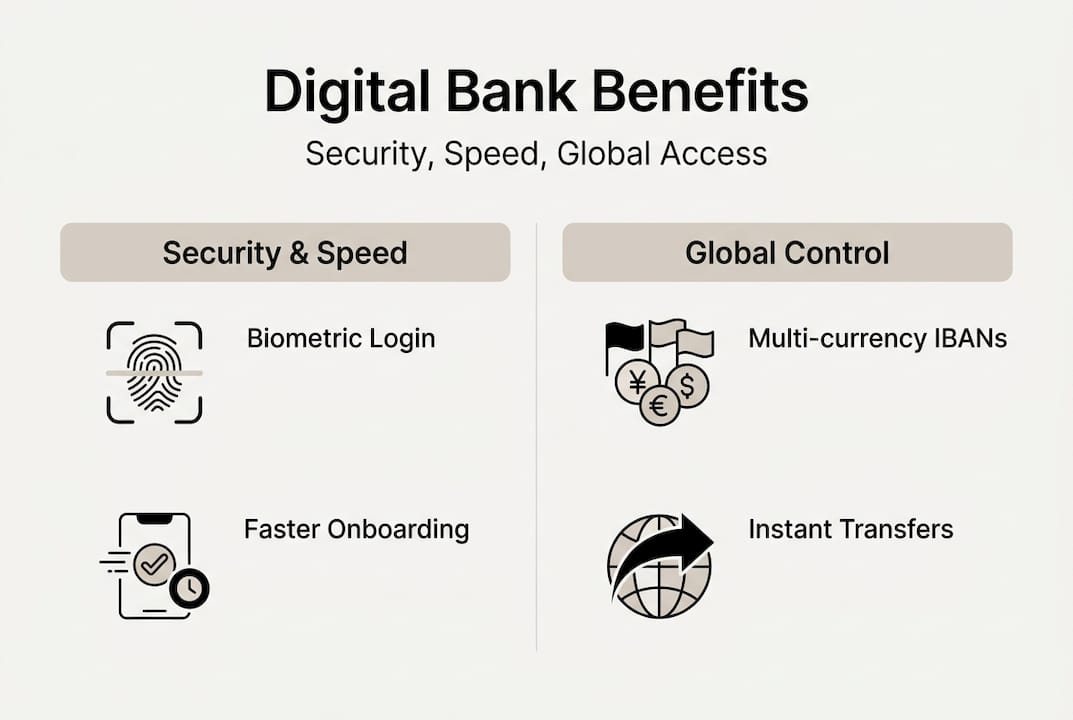

The security architecture of leading digital banks is genuinely advanced. AI fraud detection is used by 71% of digital banks compared to just 47% of traditional institutions, alongside biometric access controls and real-time transaction monitoring. For high-net-worth individuals managing significant cross-border flows, that gap in detection capability is not trivial.

Core features that matter most to sophisticated clients include:

- Multi-currency accounts with real-time conversion and consolidated reporting

- 24/7 platform access with no branch dependency or business-hours restrictions

- API integrations that connect banking infrastructure directly to corporate treasury systems

- Offshore and numbered account options for clients requiring maximum confidentiality

- Instant SWIFT and SEPA transfers without manual processing delays

Exploring digital currency options alongside traditional multi-currency accounts is increasingly relevant for clients managing diversified asset portfolios. As modern banking trends continue to evolve, the gap between digital-native and legacy providers is widening, not narrowing.

“The question is no longer whether digital banking is secure enough for serious wealth. It is whether traditional banking is agile enough for serious clients.”

Key advantages of digital banking for high-net-worth individuals and corporates

The efficiency case for digital banking is backed by hard numbers. Cost-to-income ratios for digital-only banks run between 30% and 40%, compared to 50% to 70% for traditional banks. That structural cost advantage translates directly into better pricing, faster service, and more resources allocated to technology and client support rather than branch overhead.

Speed is equally compelling. Account opening runs up to 40 times faster at digital institutions, with loan applications processed 10 times quicker. For a corporate client closing a cross-border acquisition or a high-net-worth individual repositioning assets across jurisdictions, waiting weeks for account activation is simply not acceptable.

| Feature | Digital banks | Traditional banks |

|---|---|---|

| Cost-to-income ratio | 30% to 40% | 50% to 70% |

| Account opening speed | Hours | Weeks |

| Loan processing speed | 10x faster | Standard timeline |

| Multi-currency IBAN | Standard | Limited or costly |

| API integration | Native | Often unavailable |

| 24/7 access | Always | Branch-dependent |

For international operations, the advantage compounds. Multi-currency IBANs eliminate the friction of maintaining separate accounts in each jurisdiction. Integrated SWIFT access means transfers execute without manual intervention. The account opening process at leading digital institutions is designed specifically for clients who cannot afford operational delays.

Pro Tip: If your business operates across three or more currencies or jurisdictions, a digital bank’s native API infrastructure will save your treasury team significant reconciliation time every single month. Explore tailored digital banking solutions built for exactly this level of complexity.

Risks, privacy, and regulatory realities in digital banking

Digital banking’s advantages are real, but so are the risks if you choose the wrong provider. Privacy is one area where digital banks can genuinely excel, particularly through offshore account structures and KTT-enabled accounts that provide an additional layer of confidentiality. However, privacy is only meaningful when the underlying institution is properly regulated and compliant with international AML and KYC standards.

Some high-net-worth clients continue to favor Swiss and Singapore private banks for their perceived geopolitical stability and centuries of institutional trust. That preference is understandable. But it should not be confused with a blanket superiority in security or privacy technology, where digital-native institutions frequently lead.

Key risk mitigation practices for digital banking clients:

- Verify regulatory status before onboarding. Confirm the institution’s licensing jurisdiction and oversight body.

- Require dual-authorization for all high-value transactions to prevent unauthorized transfers.

- Use secure VPNs when accessing accounts from international locations or shared networks.

- Request regular audit trails and transaction logs for corporate accounts to support internal compliance.

- Confirm deposit insurance coverage and understand the limits applicable to your account structure.

Privacy solutions such as numbered accounts are legitimate tools for clients with genuine confidentiality requirements, provided they are structured within a compliant framework. As noted in Prominence Bank’s digital banking overview, digital banking suits low-cash, API-heavy operations particularly well, while clients with very large physical cash requirements or complex credit facilities may need to evaluate hybrid approaches.

“Privacy without compliance is exposure. The strongest digital banking setups combine maximum confidentiality with verifiable regulatory standing.”

Digital versus traditional banks: Efficiency and integration for global finance

When you strip away brand perception and look at performance metrics, the data favors digital institutions at scale. Digital bank ROE reaches 13.7% compared to 8.4% for traditional banks, a gap driven by lower overhead, faster capital deployment, and technology-enabled automation. For corporate clients evaluating banking partners, that efficiency differential has direct implications for service quality and pricing.

Blockchain-based settlement and AI-driven treasury tools are enabling real-time cash visibility across multiple entities and currencies, something that in-house bank architectures at traditional institutions have struggled to replicate without significant custom development.

Where traditional banks still hold ground:

- Relationship lending for large, complex credit facilities where human judgment and long-term history matter

- Perceived institutional trust among counterparties in certain markets and industries

- Physical cash management for businesses with significant cash-handling requirements

- Regulatory familiarity in jurisdictions where legacy banks have established local relationships

The honest picture is that neither model is universally superior. Business-ready platforms at leading digital institutions now offer the treasury management, multi-entity support, and cross-border transfer capabilities that previously required a relationship with a major global bank. Corporate account options have matured significantly, closing the gap on trust and service depth.

For most high-net-worth individuals and internationally active corporations in 2026, the question is not whether to use a digital bank, but which digital bank meets the specific requirements of your financial structure.

How to evaluate and choose the right digital bank

Selecting a digital banking provider is a due diligence exercise, not a marketing decision. Given that 55% of HNW clients now rank digital capabilities as a primary selection factor, the market has responded with a wide range of providers, and quality varies significantly.

Use this checklist when evaluating any digital banking institution:

- Jurisdiction and licensing. Confirm the regulatory body, operating license, and the legal framework governing your account.

- Technology infrastructure. Assess platform uptime history, security certifications, and the maturity of their fraud detection systems.

- Security protocols. Look for biometric authentication, dual-authorization, end-to-end encryption, and real-time monitoring.

- Regulatory compliance. Verify AML and KYC processes, and confirm the institution’s track record with international regulators.

- Service scope. Ensure the bank supports your required currencies, jurisdictions, account types, and transaction volumes.

- Client support. Confirm 24/7 availability across multiple channels, with dedicated relationship management for complex accounts.

- Future-proofing. Ask about the platform’s roadmap for currency support, API upgrades, and cross-border expansion.

Pro Tip: Before committing to a digital bank for corporate treasury operations, request API documentation and run a pilot transaction series. Real-world integration testing reveals far more than any sales presentation.

For clients with complex structures, exploring exclusive digital services designed specifically for high-net-worth and institutional clients will save significant time in the evaluation process. The right provider will have clear answers to every item on this checklist without hesitation.

Unlock advanced digital banking with Prominence Bank

Armed with a clear framework for digital banking, you are ready to explore top-tier options that cater to global financial needs. Prominence Bank is built specifically for clients who require private, secure, and fully online banking with the sophistication to match complex international financial structures.

From corporate banking solutions that support multi-entity structures and cross-border treasury management, to digital currency services and premium exclusive services for high-net-worth individuals, Prominence Bank delivers the full spectrum of capabilities this guide has outlined. Account opening is streamlined, compliance is built in, and the platform is designed for clients who expect institutional-grade security without institutional-grade delays. If your financial needs have outgrown what a traditional bank can efficiently deliver, this is where the conversation starts.

Frequently asked questions

Are digital banks safer than traditional banks for large balances?

Digital banks deploy biometrics and AI fraud detection at rates significantly higher than traditional institutions, but overall safety depends on the provider’s regulatory standing, deposit insurance coverage, and operational history. Always verify these factors before transferring significant assets.

Can digital banks handle cross-border multi-currency transactions easily?

Yes. Leading digital banks offer native multi-currency IBANs and integrated SWIFT access, making global transfers and accounts straightforward for both corporate clients and high-net-worth individuals managing assets across multiple jurisdictions.

What are the biggest risks with digital-only banking?

Regulatory immaturity and inconsistent service depth are the primary risks. Always verify licensing, compliance frameworks, and the institution’s operating history before onboarding, particularly for accounts holding significant balances.

Is digital onboarding really that much faster?

Account opening runs 40 times faster at digital institutions compared to traditional banks, with loan applications processed up to 10 times more quickly, making digital onboarding a material operational advantage for time-sensitive financial decisions.