TL;DR:

- Regulated crypto bank accounts offer legal protection, full custody, and seamless fiat integration.

- Opening such accounts requires thorough documentation, source of funds proof, and compliance checks.

- Choosing regulated providers prioritizes asset safety over speed and minimizes risk of platform failure.

Wealthy individuals and global corporations are sitting on a structural advantage that most financial advisors still underestimate. Major banks entering direct crypto custody and trading for elite clients signals a fundamental shift in how serious money moves. But accessing these services is not as simple as clicking “open account.” The providers worth trusting have strict requirements, meaningful fee structures, and compliance standards that screen out casual applicants. This guide walks you through every step, from understanding what a crypto bank account actually delivers, to choosing a regulated provider, to getting your account live without costly delays.

Table of Contents

- Understanding crypto banking: What you need to know

- Requirements and preparatory steps: What documents and information are needed

- Choosing the right crypto bank: Regulated providers and cost considerations

- Step-by-step account opening process

- Our perspective: What most guides overlook about crypto banking

- Connect with leading crypto banking solutions

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Regulated banks matter | Choosing regulated providers ensures greater security and compliance for crypto assets. |

| Prepare documents early | You’ll streamline account opening by gathering IDs, corporate paperwork, and proof of funds in advance. |

| Compare fees and services | Evaluate opening costs and ongoing charges alongside advanced financial features for your needs. |

| Follow step-by-step process | Success requires completing paperwork, verification, and regulatory checks without shortcuts. |

Understanding crypto banking: What you need to know

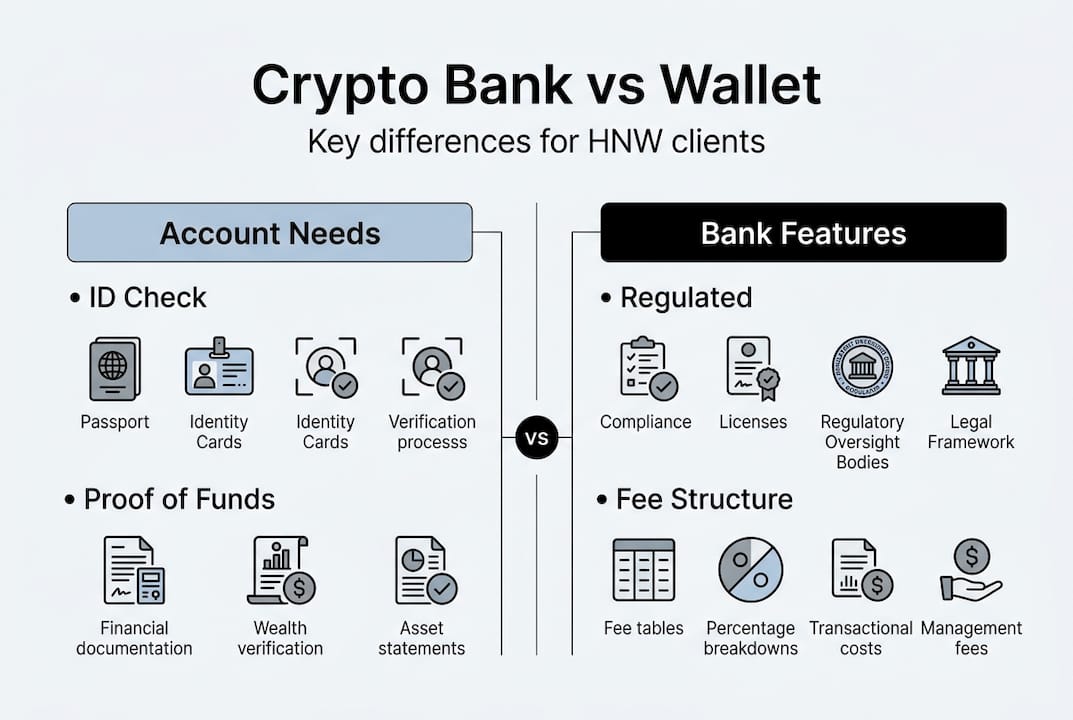

A crypto bank account is not the same as a crypto wallet. A wallet holds private keys and gives you direct control over digital assets. A crypto bank account, by contrast, is a regulated financial product where the institution holds custody of your assets, provides fiat conversion, and integrates digital currency management with traditional banking services. For high-net-worth individuals and international businesses, that distinction is everything.

The services bundled into a genuine crypto bank account typically include:

- Institutional custody with segregated asset storage

- Multi-currency trading across major digital assets and fiat pairs

- Privacy and confidentiality protections beyond standard retail banking

- Fiat on/off ramps with same-day settlement for large transfers

- Dedicated relationship management for complex corporate structures

For context, US banks now offer direct BTC trading and custody for private wealth clients, a shift that would have been unthinkable five years ago. Institutions like PNC and UBS have moved from cautious observation to active product development in this space.

Here is a quick comparison of account types to orient your decision:

| Feature | Crypto wallet | Crypto bank account |

|---|---|---|

| Custody | Self-held | Institutional |

| Regulatory protection | Minimal | Full (licensed) |

| Fiat integration | Limited | Seamless |

| Privacy level | Pseudonymous | Contractual confidentiality |

| Suitable for HNWIs | Rarely | Yes |

The regulatory protection column is where most wealthy clients make their first mistake. A self-custodied wallet offers no recourse if something goes wrong. A regulated bank account gives you legal standing, insurance frameworks, and dispute resolution. For anyone managing significant digital asset positions, that protection is non-negotiable.

If you are new to structuring international financial access, reviewing a private banking setup guide before proceeding will help you frame the right questions. Similarly, understanding the international banking benefits available to global clients will sharpen your provider selection criteria.

Requirements and preparatory steps: What documents and information are needed

With banking terminology and services clarified, let’s look at what you need to gather before applying. Banks that take crypto seriously also take compliance seriously. Expect a thorough review process, not a five-minute sign-up.

For personal accounts, you will typically need:

- Government-issued photo ID (passport preferred)

- Proof of residential address dated within 90 days

- Source of funds documentation (investment statements, sale records, inheritance documentation)

- Tax identification numbers for all relevant jurisdictions

- A completed wealth declaration or net worth statement

For corporate accounts, the list expands:

- Certificate of incorporation and articles of association

- Register of directors and beneficial owners

- Corporate resolution authorizing account opening

- Audited financial statements (last 2 years minimum)

- Proof of business activity and anticipated transaction volumes

Here is how personal and corporate requirements compare across account tiers:

| Requirement | Personal HNWI | Corporate/International |

|---|---|---|

| Photo ID | Required | Required for all directors |

| Address proof | Required | Registered office proof |

| Source of funds | Detailed | Full corporate financials |

| KYC/AML screening | Standard | Enhanced due diligence |

| Beneficial ownership | Self | Full UBO disclosure |

As the account opening requirements at regulated institutions confirm, HNWIs must expect robust KYC and AML checks as a baseline condition for asset protection, not an obstacle to it. Banks that skip these checks are the ones you should avoid.

Digital onboarding has made remote verification faster, but it has not made it less rigorous. Prepare certified copies of all documents in advance. If your assets span multiple jurisdictions, a legal apostille may be required for corporate filings.

Pro Tip: Organize all documents into a single encrypted folder before you begin any application. Incomplete submissions are the single most common reason for delays, and re-submitting documents resets your position in the review queue.

For a detailed walkthrough of the digital process, the secure online account opening resource covers what to expect at each verification stage. If you are ready to explore account options directly, the cryptocurrency bank account page outlines available structures.

Choosing the right crypto bank: Regulated providers and cost considerations

Once you are organized with the required documents, it is time to compare crypto banking alternatives for safety and cost. Not all providers are equal, and the differences matter at scale.

Regulated banks operate under licensing frameworks that require capital adequacy, client asset segregation, and independent audits. Unregulated platforms may offer faster onboarding and lower stated fees, but they carry risks that no serious wealth manager would accept: no deposit protection, no legal recourse, and exposure to sudden platform shutdowns.

Fee structures vary widely. High fees at private banks can reach €25,000 for opening, with ongoing charges layered on top. Regulated providers, by contrast, offer greater asset protection and clearer fee disclosures, so you know exactly what you are paying and why.

Here is a comparison of leading regulated crypto banking options:

| Provider | Jurisdiction | Crypto services | Typical opening fee | Regulatory status |

|---|---|---|---|---|

| Sygnum | Switzerland | Full crypto banking | High | FINMA licensed |

| AMINA | Switzerland | Custody, trading | High | FINMA licensed |

| Prominence Bank | ETMO | Multi-currency, digital assets | Competitive | Fully licensed |

| UBS (select clients) | Switzerland/Global | BTC trading (limited) | Very high | Multiple regulators |

For clients managing complex international structures, the choice between Swiss-domiciled banks and newer global entrants often comes down to flexibility. Swiss institutions carry strong reputational weight, but their onboarding timelines and minimum asset thresholds can be prohibitive. As the account opening fees details page illustrates, regulated banks such as Sygnum or AMINA offer genuine asset protection, but newer licensed entrants can provide comparable security with more accessible entry points.

The most expensive mistake in crypto banking is choosing a provider based on speed alone. Regulatory status is the only variable that protects your assets when markets move against you.

For businesses with cross-border asset exposure, reviewing asset protection abroad strategies before committing to a provider will help you structure your banking relationships for maximum resilience.

Step-by-step account opening process

Now, let’s walk through the actual steps you will need to follow to get your crypto bank account live.

-

Select your provider and account type. Based on your jurisdiction, asset size, and business structure, identify two or three regulated providers that meet your criteria. Do not apply to multiple banks simultaneously without a clear strategy, as parallel applications can trigger compliance flags.

-

Complete the online application. Most regulated crypto banks now offer fully digital onboarding. Fill out the application accurately, paying close attention to source of funds declarations. Vague answers here are the fastest route to rejection.

-

Upload your documents. Submit certified copies of all required documents through the bank’s secure portal. Ensure file quality is high and that all documents are current. Expired IDs or outdated address proofs will stall the process immediately.

-

Respond to due diligence questions. Compliance teams will often follow up with specific questions about your transaction history, business activity, or asset origins. Respond promptly and completely. Delays in responding extend your timeline proportionally.

-

Await verification and approval. The review period typically runs one to three weeks for straightforward applications. Complex corporate structures or multi-jurisdictional ownership may extend this to four to six weeks.

-

Receive account credentials and activate. Once approved, you will receive secure login credentials and onboarding instructions. Fund the account according to the minimum deposit requirements and confirm your access to all services.

PNC and UBS now offer direct crypto trading for select HNWI clients, which signals that the infrastructure for institutional-grade digital asset banking is maturing rapidly. That means more options, but also more due diligence required to separate genuine regulated offerings from marketing-heavy alternatives.

Pro Tip: Before submitting your crypto account application, have a legal or compliance advisor review your source of funds documentation. A single inconsistency between your declared wealth and your transaction history can delay approval by weeks.

Common mistakes to avoid: submitting unverified document copies, underestimating the detail required in source of funds explanations, and failing to disclose all beneficial owners in corporate structures.

Our perspective: What most guides overlook about crypto banking

Most step-by-step guides focus on the mechanics and miss the strategic layer entirely. Here is what we have observed working with high-net-worth clients and international corporations: the banks that make onboarding feel effortless are often the ones cutting corners on compliance. That should concern you.

Fee transparency is a more reliable signal of institutional integrity than any marketing claim. A bank that clearly itemizes its opening costs, custody fees, and transaction charges is a bank that respects your intelligence and your capital. One that buries fees in fine print or quotes suspiciously low headline rates is telling you something important about how it operates.

Regulatory status is not a checkbox. It is the foundation of every protection you have as a depositor. Regulated banks offer greater security for high-value crypto assets precisely because they are subject to oversight that unregulated platforms are not.

Speed is the wrong optimization target. The clients who rush into the fastest available option often find themselves rebuilding their banking relationships within 18 months. Choosing a provider with a strong private banking setup guide and genuine compliance infrastructure takes longer upfront and pays dividends indefinitely.

Connect with leading crypto banking solutions

The guidance above gives you the framework. Prominence Bank gives you the infrastructure to act on it.

As a fully licensed digital banking institution, Prominence Bank offers digital currency services designed specifically for high-net-worth individuals and international corporations that require discretion, regulatory compliance, and genuine asset protection. Our business banking solutions cover multi-currency accounts, corporate structures, and institutional-grade digital asset management. If you are ready to open a secure crypto bank account or want to discuss your specific requirements with our team, initiate your application through our online portal today.

Frequently asked questions

What documents do I need to open a crypto bank account?

You will need personal identification, proof of address, and documentation verifying your source of funds; businesses also require incorporation documents and beneficial ownership disclosures.

How much are the typical fees for opening a crypto bank account?

Private banks may charge up to €25,000 for opening; regulated institutions typically provide greater asset protection and clearer fee structures that justify the cost.

How long does it take to open a crypto bank account?

The process usually takes one to three weeks, though complex corporate structures or multi-jurisdictional ownership can extend verification timelines to four to six weeks.

Are crypto bank accounts available internationally?

Yes, regulated banks are expanding crypto account offerings to eligible international clients, including corporations and high-net-worth individuals across multiple jurisdictions.