TL;DR:

- Private banking requires careful preparation, documentation, and understanding of bank evaluation criteria.

- Different client tiers demand varying minimum assets and offer tailored services from basic to ultra-high-net-worth clients.

- Hybrid models and family offices provide advanced privacy, control, and customization beyond standard private banking.

Banking privacy is not a luxury for high-net-worth individuals and global corporations. It is a strategic necessity. As regulatory complexity grows and financial institutions tighten access, securing a private banking relationship that matches your profile, jurisdiction, and goals requires more than a large balance. It demands preparation, the right documentation, and a clear understanding of how banks evaluate clients. This guide walks you through every stage of the setup process, from eligibility and documentation to advanced structures like family offices and hybrid models, so you can move forward with confidence and avoid the most common pitfalls.

Table of Contents

- Understanding private banking: Core features, client profiles, and minimums

- Preparing for private banking: Key documents, eligibility hurdles, and what banks scrutinize

- The setup process: From selection to account activation

- Beyond basics: Hybrid models, family offices, and customization for ultimate privacy and control

- What most guides overlook: Personalization and pitfalls in private banking

- Next steps: Secure your private banking needs with expert support

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Stringent requirements | Private banking often requires $250K-$10M+ and thorough documentation for approval. |

| Complex setup | The onboarding process involves multiple steps and can take up to 12 weeks for completion. |

| Customization matters | Choosing between a private bank, hybrid, or family office depends on your wealth level and privacy needs. |

| Documentation is critical | Clear source-of-wealth proof and complete paperwork speed up approvals and reduce risk of rejection. |

| Broader options available | Advanced solutions like family offices and hybrid models provide added control for ultra-wealthy or complex needs. |

Understanding private banking: Core features, client profiles, and minimums

Private banking is not simply a premium version of your retail checking account. It is a dedicated financial service model where a bank assigns a relationship manager to your account, provides customized investment management, estate planning, tax optimization, lending, and in many cases, a family office lite structure. The distinction from standard wealth management is significant: private banking integrates multiple financial disciplines under one roof, tailored to your specific situation.

Banks segment their private clients into four broad tiers. Entry-level high-net-worth individuals typically hold investable assets between $250,000 and $1 million. Mid-tier clients range from $1 million to $5 million. Premium clients fall between $5 million and $10 million. And ultra-high-net-worth clients hold $10 million or more, accessing the most exclusive services and dedicated teams. According to private banking requirements, setup for HNWI typically requires minimum investable assets ranging from $250K to $1M for entry-level, scaling to $10M or more for ultra-high-net-worth services.

| Tier | Asset range | Core services | Due diligence |

|---|---|---|---|

| Entry-level | $250K to $1M | Basic investment mgmt, lending | 6 to 8 weeks |

| Mid-tier | $1M to $5M | Full investment suite, tax planning | 8 to 10 weeks |

| Premium | $5M to $10M | Estate planning, credit facilities | 10 to 12 weeks |

| Ultra-HNW | $10M+ | Family office, bespoke lending | 12+ weeks |

For international corporations, private banking offers a different value proposition. Treasury integration, multi-currency access, cross-border lending, and consolidated reporting are the priorities. The private banking overview at Prominence Bank illustrates how corporate clients can access these services within a fully digital, privacy-focused framework.

When selecting a bank, the factors that matter most include service quality, investment philosophy, geographic coverage, and institutional stability. As noted in how to choose a private bank, bank selection criteria should be driven by your specific financial goals and risk profile, not by brand recognition alone.

- Investment management: Discretionary and advisory mandates

- Estate and succession planning: Cross-border asset transfer strategies

- Tax optimization: Jurisdiction-specific structures and reporting

- Lending and credit: Lombard loans, real estate financing, bridge credit

- Corporate treasury: Multi-currency accounts, FX hedging, liquidity management

Preparing for private banking: Key documents, eligibility hurdles, and what banks scrutinize

Passing a private bank’s due diligence process is where most applicants stumble. Banks are not just evaluating your wealth. They are evaluating the clarity, legitimacy, and traceability of that wealth. Preparation here is not optional. It is the difference between a smooth onboarding and a rejection letter.

The core documents you need include:

- Government-issued photo identification (passport preferred)

- Proof of address dated within 90 days

- Certified financial statements for the past two to three years

- Tax returns or equivalent tax compliance documentation

- Source of wealth narrative with supporting evidence

- For corporations: articles of incorporation, shareholder registry, beneficial ownership declarations, and audited accounts

KYC (Know Your Customer) and AML (Anti-Money Laundering) checks form the backbone of bank due diligence. For cross-border applicants, enhanced KYC/AML scrutiny significantly increases timelines, and banks will probe the origin of every major asset or income stream. The open account process at Prominence Bank is streamlined for international clients, but the underlying compliance requirements remain rigorous.

For international applicants, expect the due diligence window to extend beyond standard timelines if your corporate structure spans multiple jurisdictions or includes entities in flagged regions. Prepare a clean, narrative-driven source of wealth document before you submit anything.

Common causes for rejection or delay include unclear documentation, complex multi-layered ownership structures, connections to sanctioned jurisdictions, and inconsistencies between declared income and asset values. Banks also flag clients with prior regulatory issues or those who cannot clearly explain a major liquidity event.

Flexibility does exist. Below-minimum exceptions are sometimes granted for high-growth potential clients or those with existing relationships at the institution. But disqualifiers like regulatory violations or an unclear source of wealth are rarely negotiable.

Pro Tip: Before approaching any private bank, prepare a one to two page source of wealth summary. Treat it like an executive brief. It should explain your wealth origin, key liquidity events, and current asset structure in plain language. Banks appreciate clients who make due diligence easy.

The setup process: From selection to account activation

With your documents organized and your source of wealth story clear, the actual setup process becomes far more manageable. The key is sequencing your steps correctly and choosing the right institution for your profile.

Bank selection is the first critical decision. Global banks like JPMorgan and Goldman Sachs typically require $10M or more, while traditional private banks like UBS operate with minimums around $3 million to $5 million. A decision framework built on four steps, defining your needs, assessing your profile, researching institutions, and evaluating fit, will help you narrow your options without wasting time on banks that are a poor match.

| Bank type | Typical minimum | Strengths | Best for |

|---|---|---|---|

| Global (JPM, GS) | $10M+ | Full-service, global reach | UHNW, institutional |

| Traditional (UBS) | $3M to $5M | Investment depth, estate planning | Premium HNW |

| Digital private banks | $250K to $1M | Speed, privacy, online access | Entry to mid-tier |

Here is the step-by-step sequence for private bank setup steps:

- Define your financial objectives and required service scope

- Assess your asset profile and confirm you meet minimum thresholds

- Research two to three banks that match your profile and jurisdiction

- Schedule initial consultations and present your financial overview

- Submit your full documentation package

- Attend bank interviews or relationship manager meetings

- Allow the due diligence period to complete (typically 6 to 12 weeks)

- Review and sign account agreements

- Fund the account to meet the required minimum

For corporations, secure corporate banking structures require additional steps around beneficial ownership verification and treasury integration planning.

Pro Tip: Never rely on a single banking relationship. Build multi-jurisdiction resilience by maintaining accounts at two institutions with different geographic footprints. If one bank faces regulatory disruption or de-risking pressure, your financial continuity is protected.

Beyond basics: Hybrid models, family offices, and customization for ultimate privacy and control

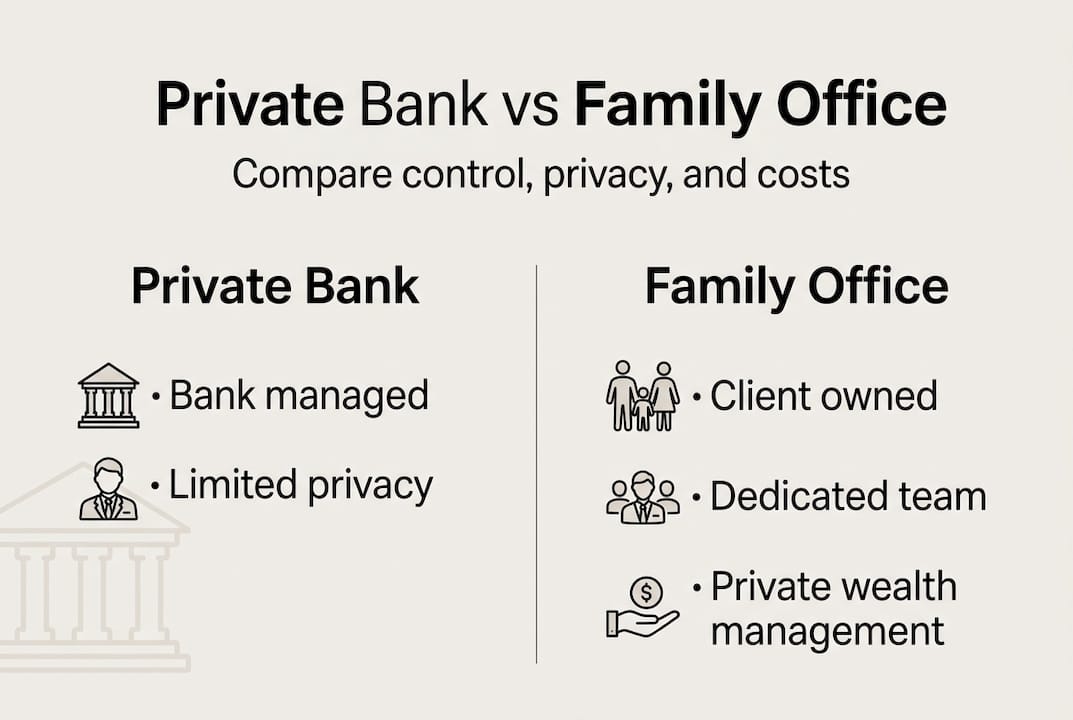

For clients whose needs exceed what a standard private banking relationship can deliver, the next tier of structures offers significantly greater control, privacy, and customization. The three models to understand are private banks, family offices, and hybrid arrangements.

A private bank provides scalable access to wealth management services, but the level of customization is limited by the bank’s own product range and risk appetite. Fees typically range from 0.5% to 2% of assets under management, and the client operates within the bank’s framework rather than their own.

A family office, by contrast, is a dedicated structure that the client owns and controls. Single-family offices (SFO) serve one family exclusively, while multi-family offices (MFO) pool resources across several ultra-wealthy families. Family office costs average 31 to 42 basis points of AUM, but total operating costs often exceed $1 million per year, making them practical only above approximately $250 million in assets. The setup process involves clarifying objectives, choosing the right structure, building a professional team, and establishing governance through a family charter.

| Structure | Asset minimum | Control | Privacy | Annual cost |

|---|---|---|---|---|

| Private bank | $250K to $10M+ | Low to medium | Medium | 0.5% to 2% AUM |

| Family office | $250M+ | High | Very high | $1M+/yr |

| Hybrid model | $50M to $250M | Medium to high | High | Variable |

Hybrid models blend private bank infrastructure with family office governance. They are ideal for clients in the $50 million to $250 million range who need more customization than a private bank offers but are not yet at the scale to justify a full SFO. For multinational families and enterprises, the discreet banking capabilities of a hybrid model can be structured around specific jurisdictions and reporting requirements.

Before moving beyond standard private banking, ask yourself:

- Do my needs require investment decisions outside a bank’s standard product shelf?

- Is multi-generational wealth transfer a priority requiring dedicated governance?

- Do I need consolidated reporting across more than three jurisdictions?

- Is the cost of a family office justified by the complexity of my holdings?

- Would a family office governance setup improve accountability across my enterprise?

What most guides overlook: Personalization and pitfalls in private banking

Most clients approach private banking by chasing brand names. They assume that the largest, most recognized institution is automatically the best fit. That assumption is expensive. The world’s biggest private banks are optimized for scale, not for the nuanced needs of a mid-tier client with a complex corporate structure or a cross-border family situation.

Real advantage comes from matching your profile precisely to the right level of service. A client with $3 million in assets and a clean, simple structure may be far better served by a boutique digital private bank than by a global institution where they will be a low-priority account.

The most consistent pitfalls we see are underestimating documentation requirements, relying on a single banking relationship, and neglecting governance structures like family charters until a crisis forces the issue. These are not minor oversights. They create delays, expose vulnerabilities, and in some cases, result in account closures.

The clients who succeed long-term treat their banking relationship as an active, evolving partnership. They invest in privacy and discretion structures proactively, not reactively. The best private banking relationships are built over years, not activated in a single onboarding call.

Next steps: Secure your private banking needs with expert support

You now have a clear framework for evaluating your eligibility, preparing your documentation, selecting the right structure, and understanding when to move beyond standard private banking. The next step is finding an institution built to serve your specific profile.

Prominence Bank offers fully digital, privacy-focused solutions for high-net-worth individuals and international corporations. From digital currency solutions and corporate banking to premium private banking services designed for demanding global clients, the platform is built for those who require speed, discretion, and global access. Contact our specialists today for a tailored consultation and take the first step toward a banking structure that works as hard as you do.

Frequently asked questions

What is the minimum amount required to open a private bank account?

Most private banks require at least $250,000 to $1 million at entry level, with higher tiers unlocking premium and ultra-high-net-worth services.

How long does it take to set up a private banking relationship?

The full process, including due diligence of 6 to 12 weeks, typically takes between two and four months from initial consultation to account activation.

What are the most common reasons private bank applications are rejected?

Applications are most often declined due to an unclear source of wealth, incomplete documentation, or corporate structures that include entities in sanctioned or flagged jurisdictions.

How are family offices different from private banks?

Family offices give clients direct ownership and control over their financial governance, while private banks operate within their own product and risk framework. Family offices cost more than $1M per year but deliver far greater customization for complex, multi-generational needs.

Can international corporations use private banking for global treasury management?

Yes. Many private banks and hybrid solutions support multinational treasury integration, including multi-currency accounts, FX management, and consolidated cross-border reporting.